At Raisegate, we have observed a striking divergence between what founders think matters and what investors actually do.

To understand this, it helps to look at how fundraising used to work. In the 1960s, bankers executing acquisitions would rent actual physical rooms in Manhattan, fill them with cabinets of contracts and audits, and make buyers sit there under supervision to read them. Today the room is just a URL, but the underlying psychology is identical. The default state of an investor is distracted.

By 2026, the data shows this distraction has evolved into brutal efficiency. The average seed pitch deck now receives exactly one minute and fifty six seconds of total viewing time. This represents a 24 percent drop in attention since 2021. If an investor spends less than two minutes on your deck, they have screened it and passed. If they spend more than four minutes, you have a strong signal of genuine interest.

But the way they spend those two minutes is counterintuitive. The old rule of thumb was that investors spend twelve to fifteen seconds per slide. That average is completely dead. Think of reviewing pitch decks as a venture capitalist's version of a dating application, except they are not looking for a match. They are actively hunting for a reason to swipe left. Because of this, reading patterns are now heavily bimodal. An investor will either skim a slide in under five seconds or settle in for a deep read of thirty to sixty seconds.

Where do they do the deep reading? They look at the financial model, the go to market motion, and the competitive positioning.

The team slide is a fascinating anchor. In 2026, the team slide receives the most total viewing time of any slide in successfully funded decks. It is also the exact only slide that appears in 100 percent of them. Investors are placing an enormous premium on the people actually building the product.

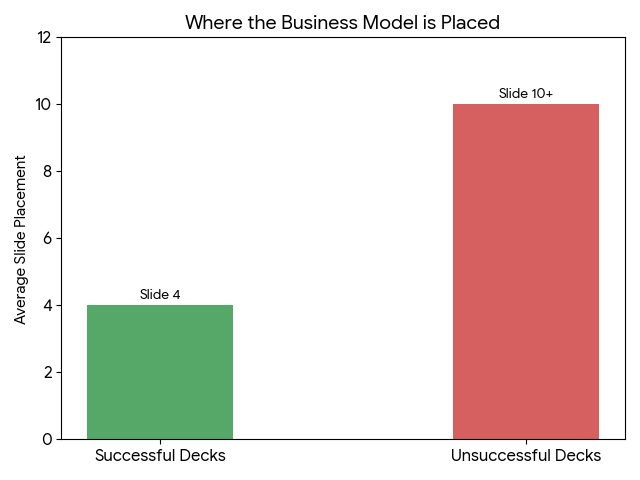

What happens to the decks that fail is perhaps the most revealing detail of all. You might assume an investor simply closes a bad deck and moves on. Instead, unsuccessful decks actually record more total time spent on their traction and business model slides. As Marc Andreessen famously put it, "Investors are not looking for a reason to say yes. They are looking for a reason to say no." The investors are not reading to be convinced. They are digging to find the exact structural flaw that justifies a pass.

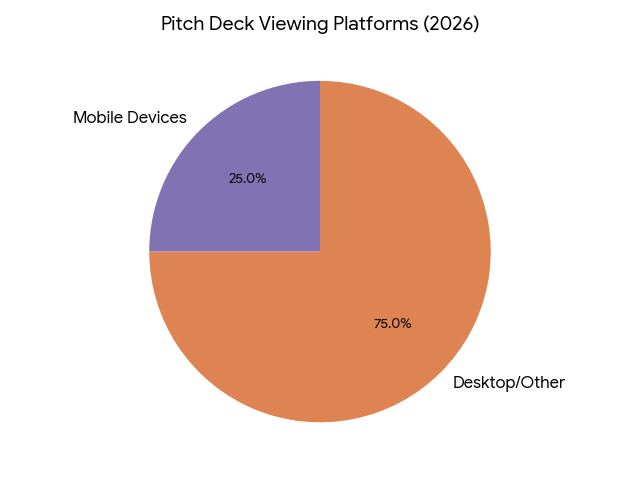

Because attention is so scarce, the architecture of your story dictates your survival. If you want to prevent an investor from dropping off, you have to front load the narrative. The first three slides must cover the problem, your traction, and your team. Successfully funded decks typically place their business model on the fourth slide. Unsuccessful founders treat monetization as an afterthought and bury it on the tenth slide or later. And since 20 to 30 percent of all pitch decks are now read primarily on mobile devices, if your fourth slide is a dense wall of text, you have already lost.

The way founders handle follow ups is also broken. The strongest indicator of a second meeting is not a long first read, but a return visit within 48 hours. When a partner likes a deck, they forward it to their team, and the second viewer now typically appears within six to ten hours. Founders should not follow up immediately after the first read. If your deck does not survive a 24 hour cooling off period, sending an email is unlikely to save it. You have to wait for that second read.

This leads to a final point about how founders behave. When fundraising gets hard, the natural instinct is to simply contact more people. It feels like a numbers game. But the data confirms there is absolutely no correlation between the sheer number of investors you contact and the total dollars you raise.

Brute force outreach does not work. Hitting send on a thousand emails merely creates the illusion of progress. To actually raise money, you have to stop trying to reach everyone, front load your best evidence, and start figuring out how to reach the exact right people.

Citations

- DocSend: What to include when building your pre-seed pitch deck

- Harvard Business Review: Venture Capital

Disclaimer: If any data is wrong or copyrighted, please DM hey@raisegate.com.